Mortgage & Loan Info

Can I Invest in a Property as a Student: A Complete Guide

Mortgage & Loan Info

What Is Negative Equity and How to Avoid It in Today’s Market

Mortgage & Loan Info

Conditional Approval Explained: Why Mortgage Deals Fall Apart (And How to Avoid It)

Mortgage & Loan Info

Average Home Closing Cost in Austin

Mortgage & Loan Info

How Much House Can I Afford With a 90K Salary

Mortgage & Loan Info

Tips To Prepare Finances To Buy A House In 2027

Mortgage & Loan Info

Important Factors To Decide Where You Should Live

Mortgage & Loan Info

When Is The Right Time To Buy A House

Mortgage & Loan Info

Top 10 Mistakes That Cost Homebuyers $10K+ (And How to Avoid Them)

Mortgage & Loan Info

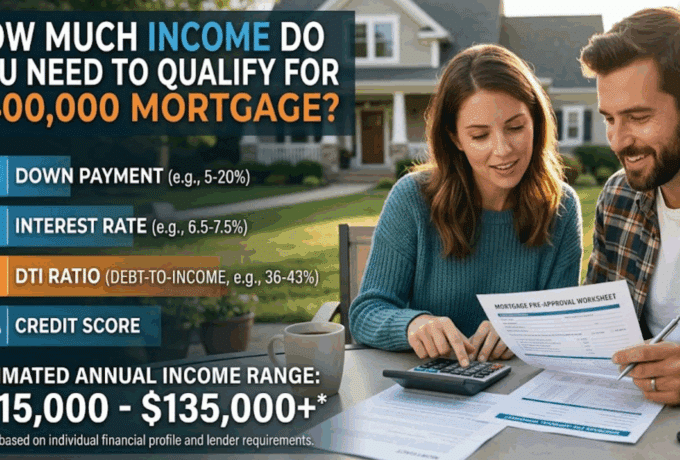

How Much Income Do You Really Need to Afford a $500k – $2M Home

Mortgage & Loan Info

How to Qualify for a Mortgage With High Debt-to-Income (DTI)

Mortgage & Loan Info

How to Get a Mortgage If You’re Self-Employed

Mortgage & Loan Info

DSCR Loans Explained: How Investors Qualify Without Income

Mortgage & Loan Info

How Much Cash You REALLY Need to Close & How to Reduce it

Mortgage & Loan Info

Can You Really Buy a $1M Home With 10% Down? : Jumbo Loan Breakdown

Mortgage & Loan Info

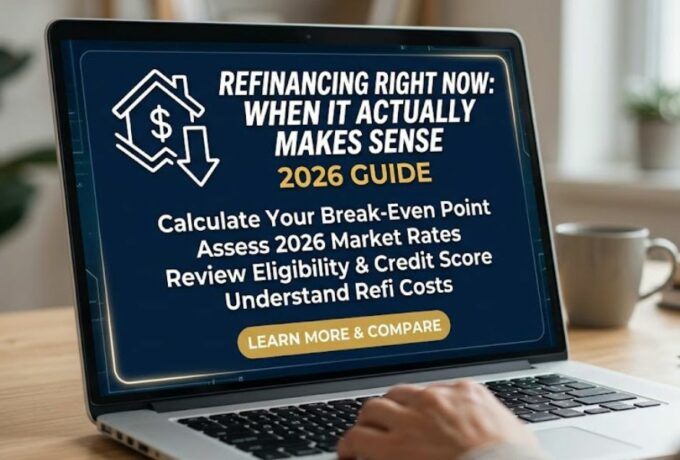

Refinancing Right Now: When It Actually Makes Sense: 2026 Guide

Mortgage & Loan Info

Bank Statement Loans vs Traditional Loans

Mortgage & Loan Info

What Happens If Mortgage Rates Drop After You Buy?

Mortgage & Loan Info

Types Of Home Loans & Mortgages

Mortgage & Loan Info

What Is Debt To Income Ratio: A Complete Guide

Mortgage & Loan Info

Jumbo Loan Rates 2026: A Complete Guide

Mortgage & Loan Info

What Is Loan To Value Ratio: A Complete Guide

Mortgage & Loan Info

What Salary Do You Need to Buy a $250K Home?

Mortgage & Loan Info

What Salary Is Required to Qualify for a $200,000 Home Loan

Mortgage & Loan Info

How to Qualify for a Mortgage with Student Loans

Mortgage & Loan Info

Refinancing Fees Breakdown: A Complete Guide

Mortgage & Loan Info

Are Refinance Rates Expected to Go Down Soon?

Mortgage & Loan Info

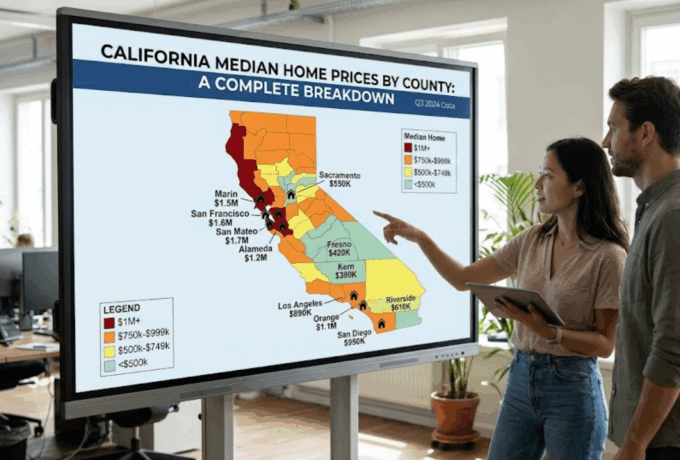

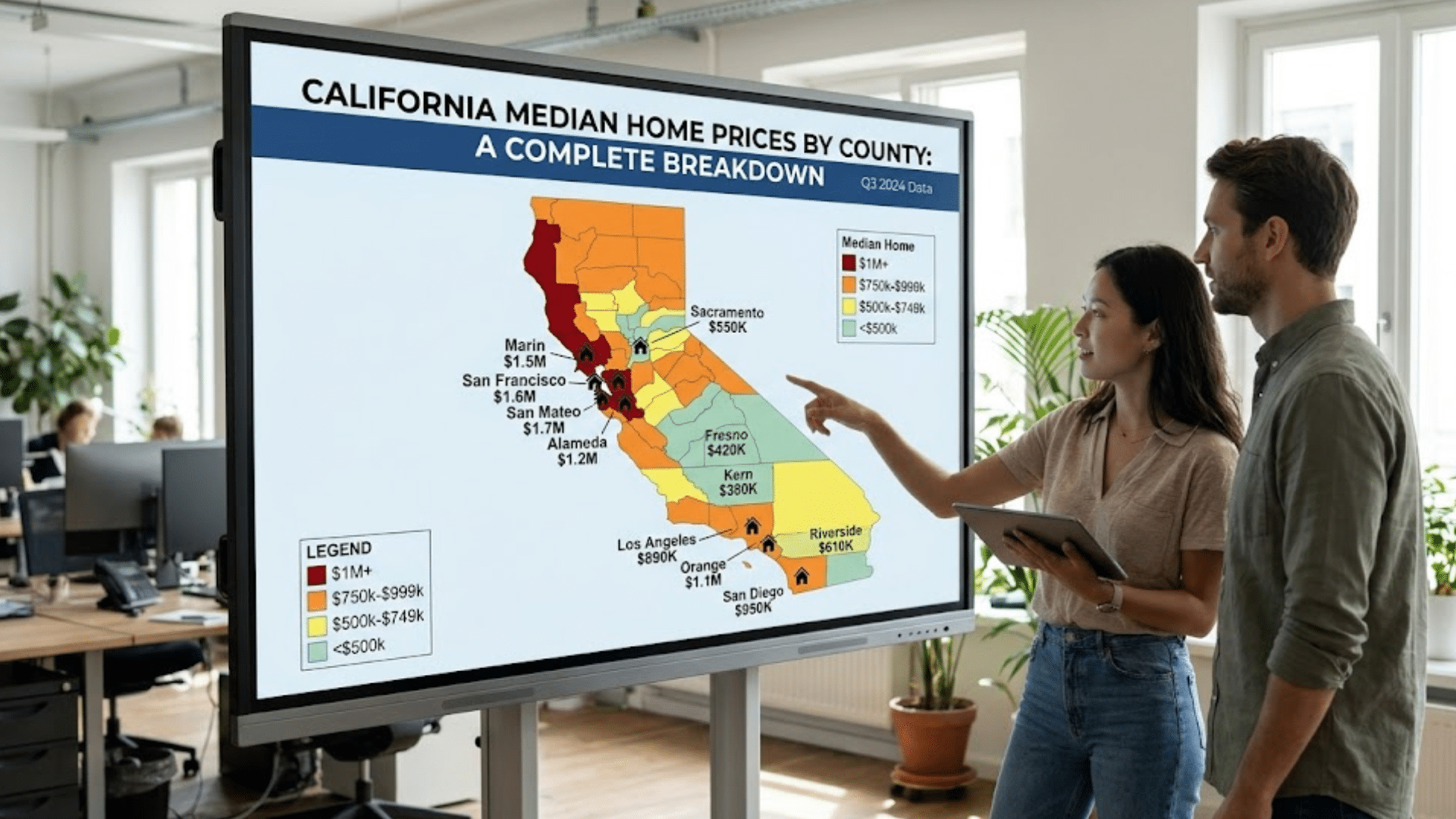

California Median Home Prices by County: A Complete Breakdown

Mortgage & Loan Info

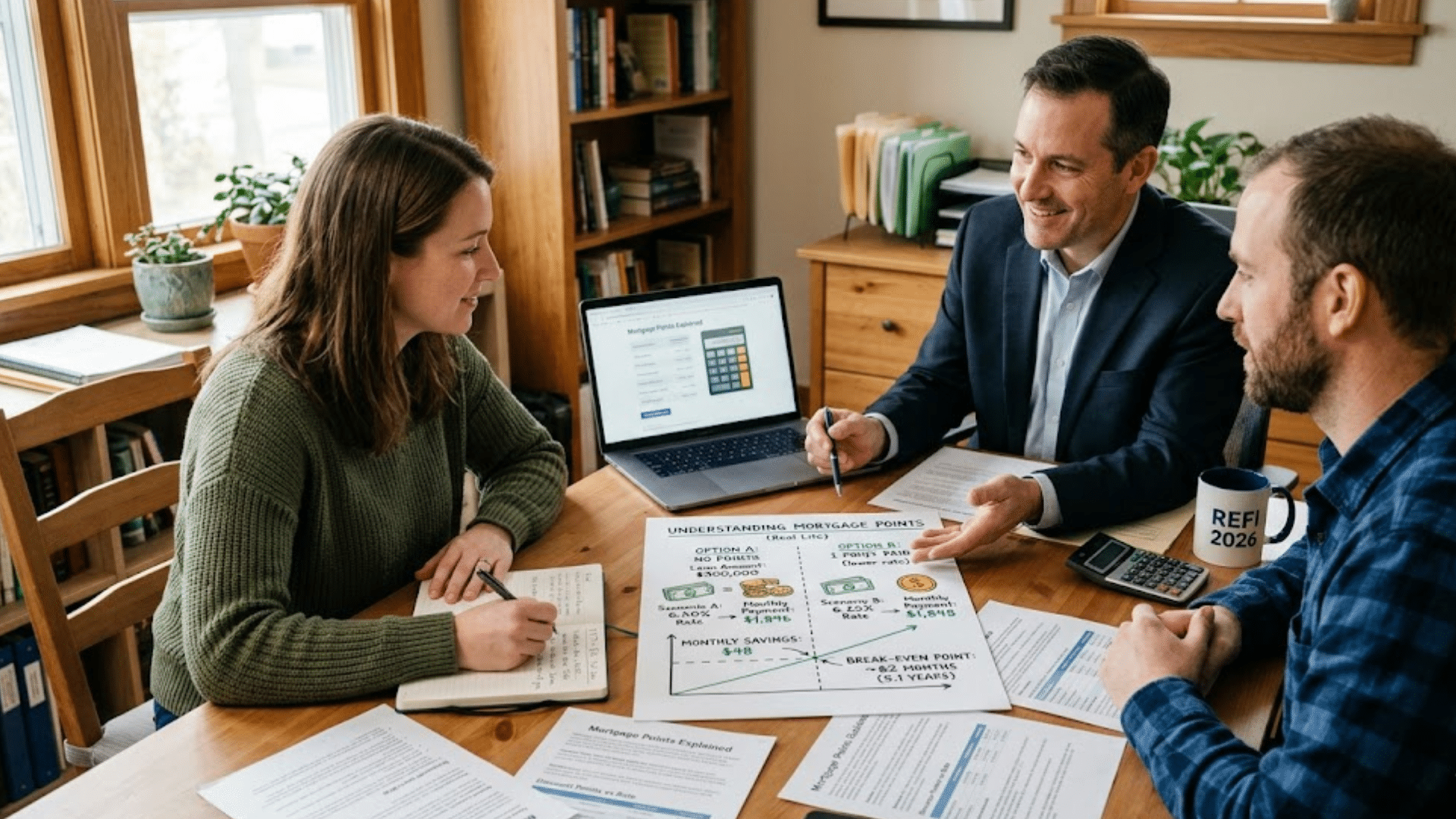

What Are Mortgage Points & How Do They Work

Mortgage & Loan Info

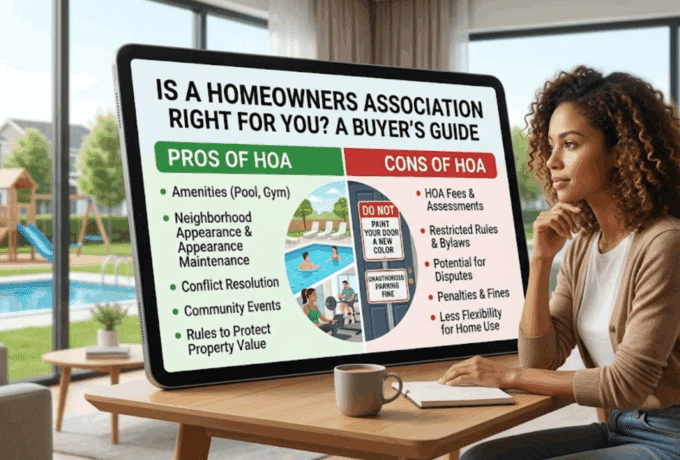

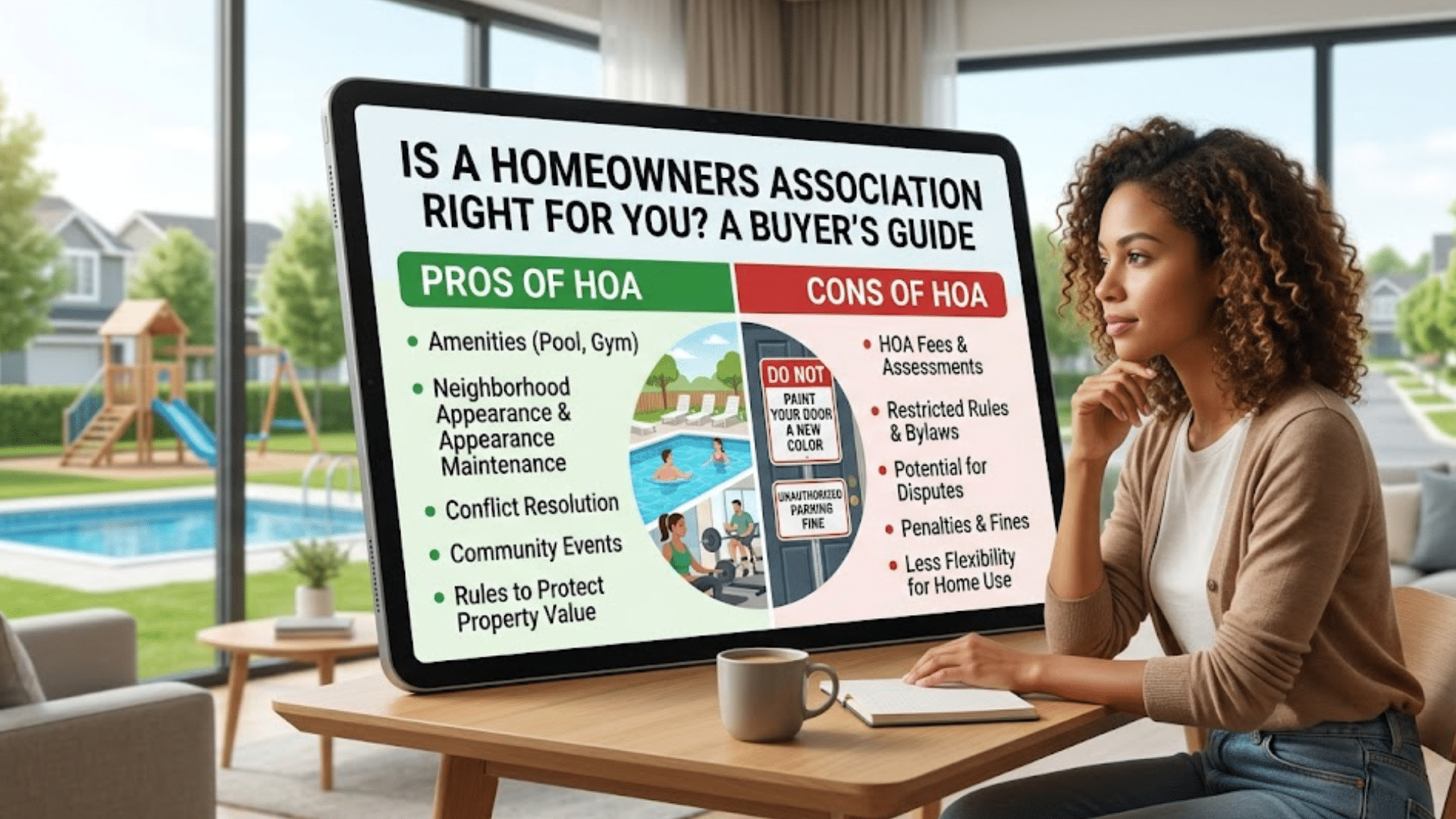

Is a Homeowners Association Right for You? A Buyer’s Guide

Mortgage & Loan Info

Mortgage Refinancing Checklist 2026

Mortgage & Loan Info

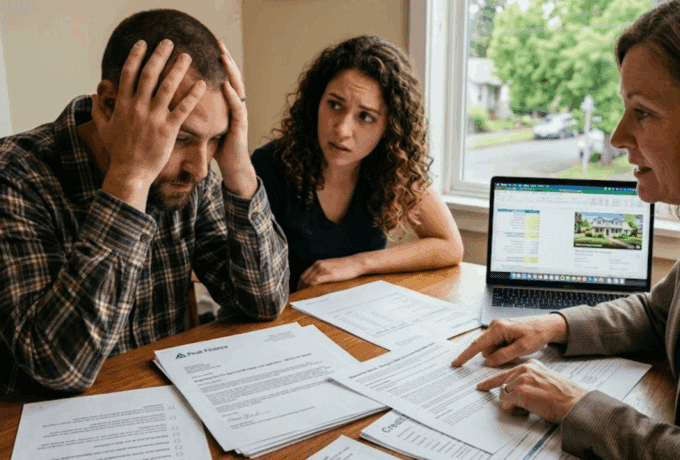

Why Lenders Deny Loans After Pre-Approval: What Homebuyers Need to Know

Mortgage & Loan Info

Are H1B Visa Holders Eligible for FHA Loans? Find Out if You Qualify

Mortgage & Loan Info

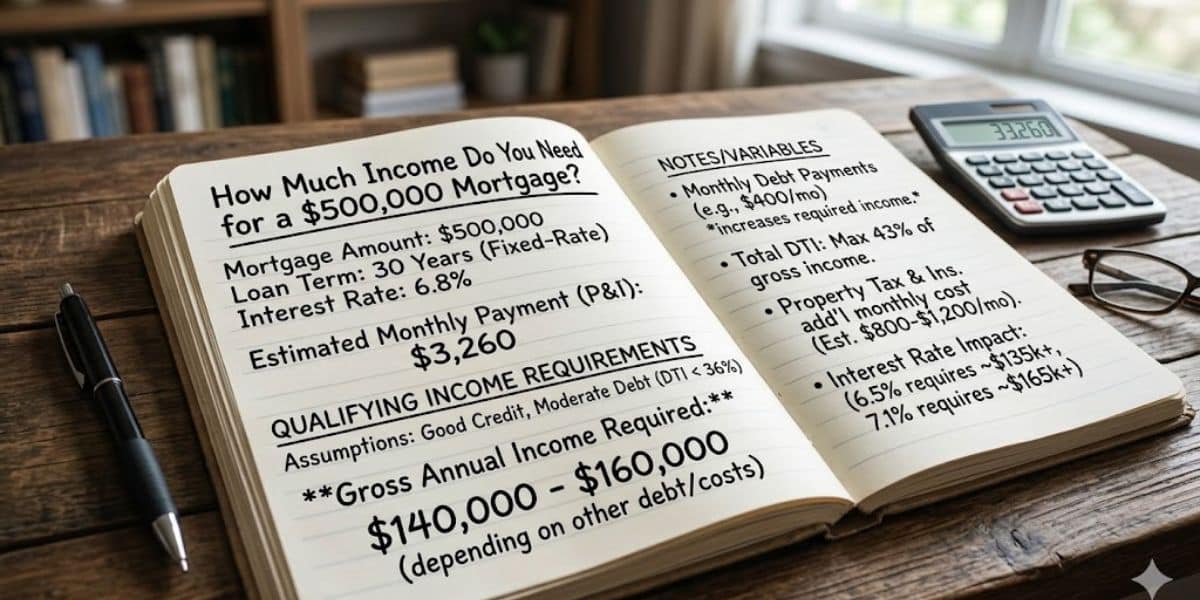

How Much Income Do You Need for a $500,000 Mortgage?

Mortgage & Loan Info

What Price Home Can You Buy With a $70,000 Salary?

Mortgage & Loan Info

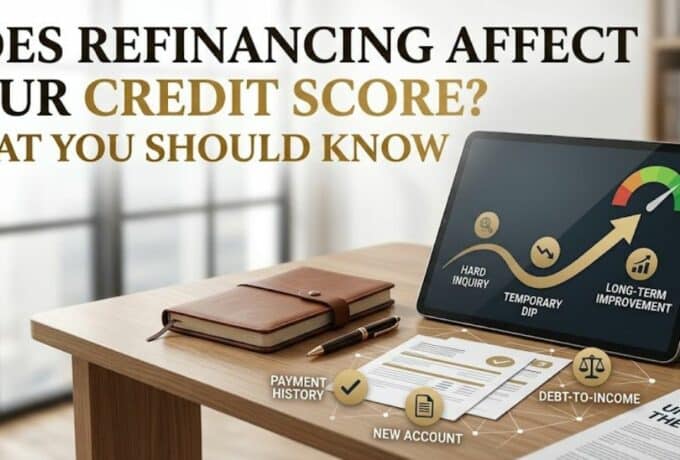

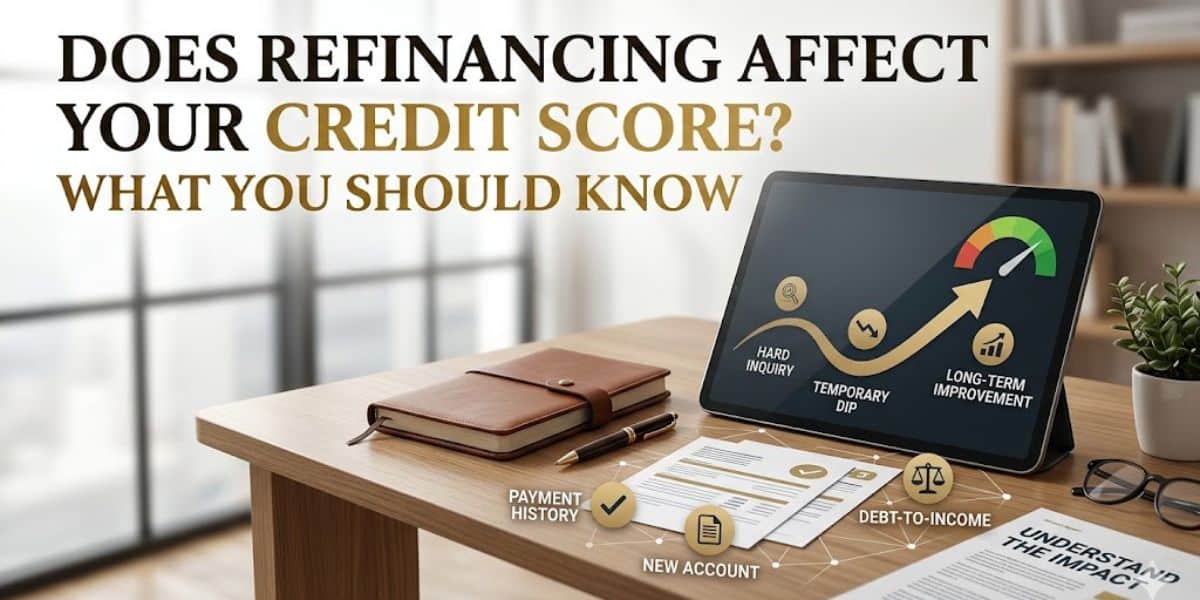

Does Refinancing Affect Your Credit Score? What You Should Know

Mortgage & Loan Info

Non QM Home Loan Rates United States 2026

Mortgage & Loan Info

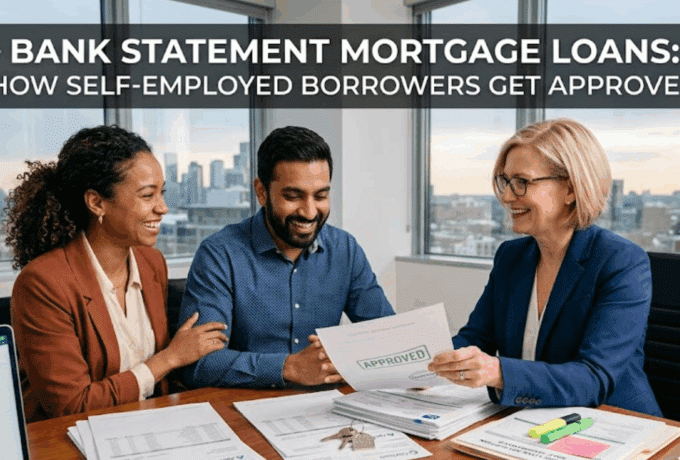

Bank Statement Mortgage Loans: How Self-Employed Borrowers Get Approved

Mortgage & Loan Info

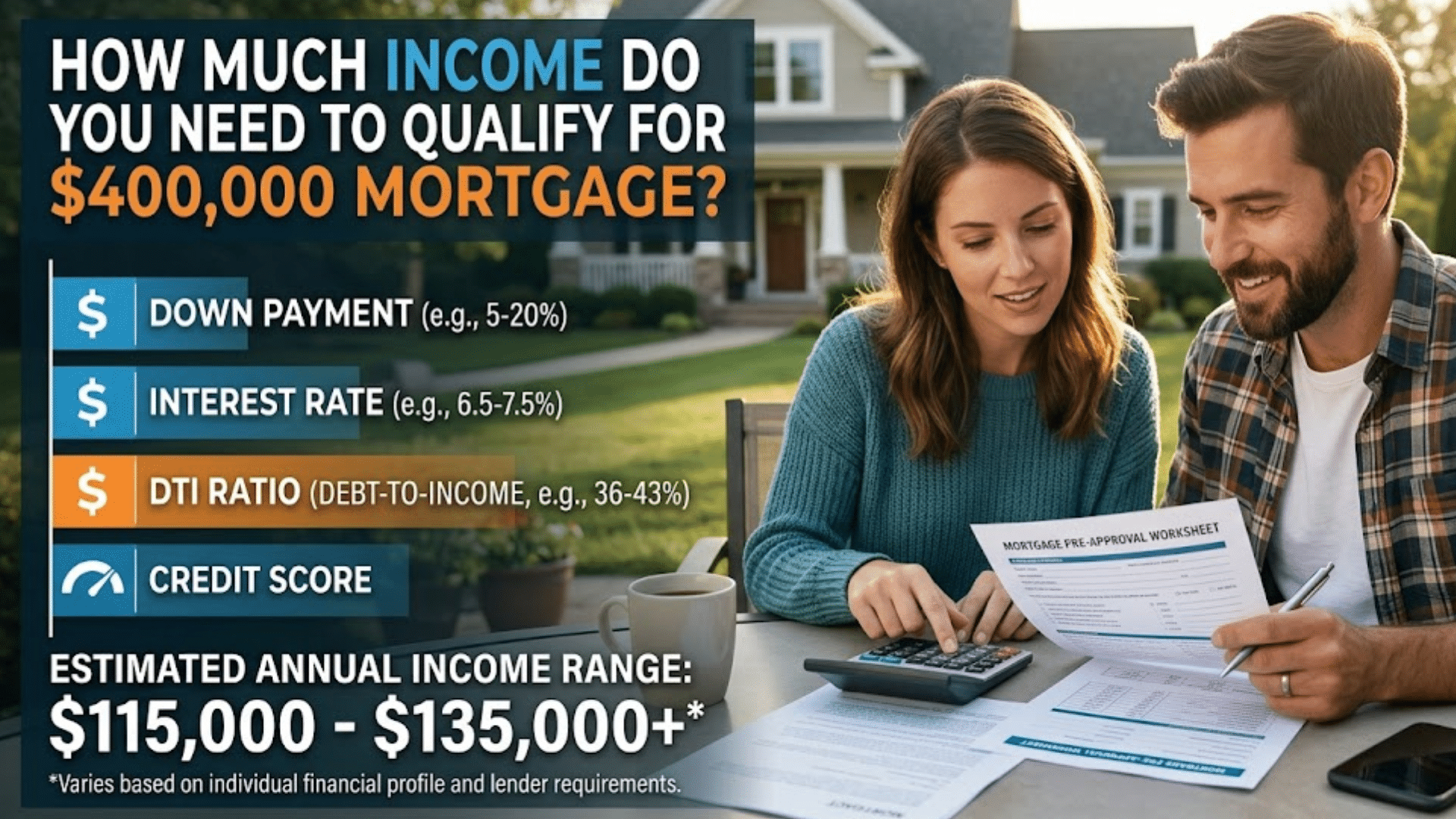

How Much Income Do You Need to Qualify for a $400,000 Mortgage?

Mortgage & Loan Info

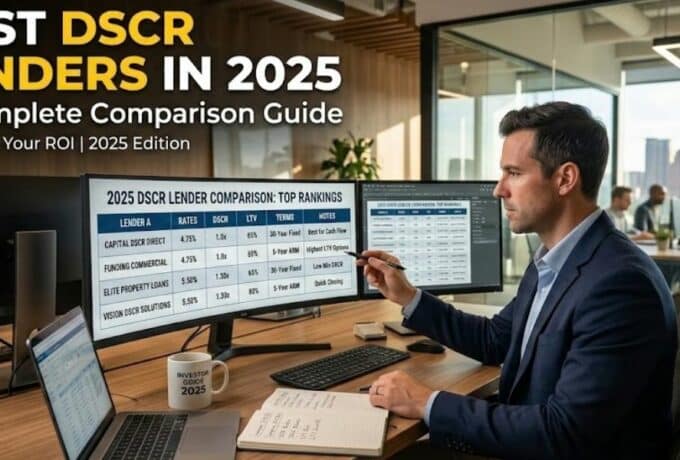

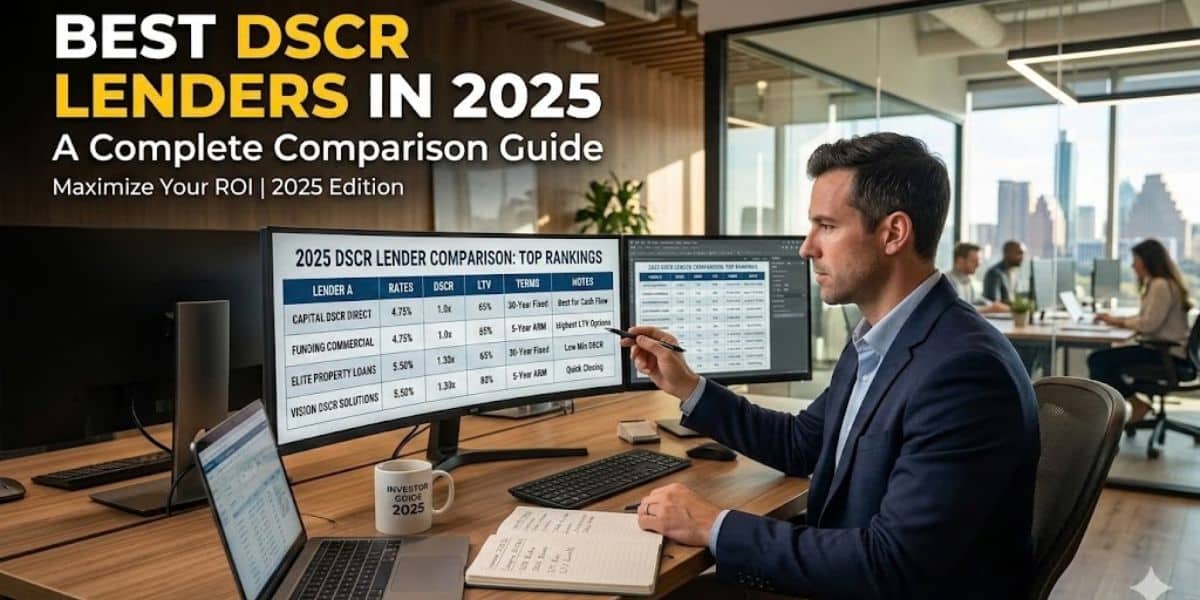

Best DSCR Lenders in 2025: A Complete Comparison Guide

Mortgage & Loan Info

Cash-Out Refinance Rates 2026: 30-Year, FHA, VA, and Non-QM Explained

Mortgage & Loan Info

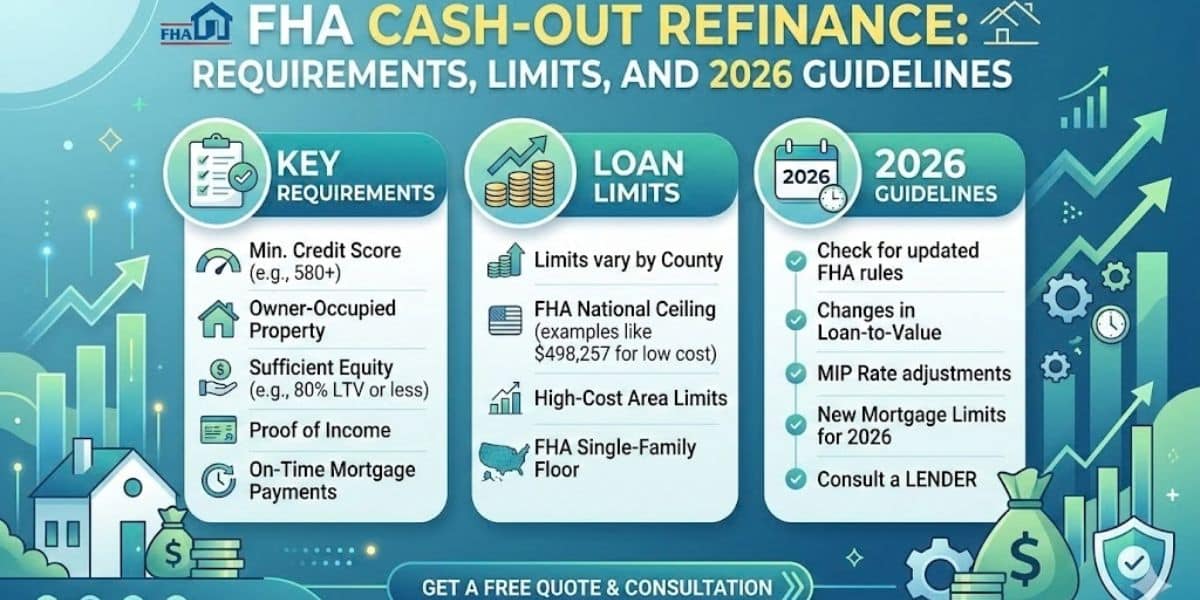

FHA Cash-Out Refinance: Requirements, Limits, and 2026 Guidelines

Mortgage & Loan Info

DSCR Loans Explained: The Ultimate 2026 Investor’s Guide

Mortgage & Loan Info

Cash-Out Refinance: How It Works, Requirements, and 2026 Strategies

Mortgage & Loan Info

How Much Income Do You Need to Qualify for a $300,000 Mortgage?

Mortgage & Loan Info

VA Cash-Out Refinance Eligibility, Loan Limits, and 2026 Benefits

Mortgage & Loan Info

Home Affordability on a $100K Income Explained

Mortgage & Loan Info

Non Qualified Mortgage Loan: The Complete 2026 Guide

Mortgage & Loan Info

Are Mortgage Points Tax Deductible in 2026?

Mortgage & Loan Info

Top 5 Myths About Reverse Mortgages

Mortgage & Loan Info

How Much House Can I Afford in 2026?

Mortgage & Loan Info

Best Mortgage Lenders in CA for 2026

Mortgage & Loan Info

How to Pay Off a Mortgage in 5 Years: A Step by Step Guide to Financial Freedom

Mortgage & Loan Info

What Does Entitlement Mean On A Mortgage Loan

Mortgage & Loan Info

What Are Mortgage Backed Securities

Mortgage & Loan Info

What Is A Jumbo Mortgage Loan

Mortgage & Loan Info

How To Pay Off Your Mortgage Faster

Mortgage & Loan Info

Is Mortgage Interest Tax Deductible

Mortgage & Loan Info

Cash Out Refinance vs HELOC: Which Makes More Sense

Mortgage & Loan Info

Why Do Mortgage Payments Go Up

Mortgage & Loan Info

Best Low Down Payment Home Loans For 2026

Mortgage & Loan Info

How To Determine Mortgage Payments

Mortgage & Loan Info

What are Second Home Mortgage Rates

Mortgage & Loan Info

What Is Average Mortgage Rate?

Mortgage & Loan Info

Current FHA Mortgage Rates

Mortgage & Loan Info

How Soon Can You Refinance Your Home

Mortgage & Loan Info

What Are Navy Federal Mortgage Rates

Mortgage & Loan Info

How Much Does It Cost To Refinance A 30-Year Fixed Mortgage?

Mortgage & Loan Info

Current VA Home Loan Rates

Mortgage & Loan Info

How Much VA Loan Can You Afford

Mortgage & Loan Info

How Business Owners Can Buy Homes Without Tax Returns

Mortgage & Loan Info

Refinance Rates For Homes in Fall 2025

Mortgage & Loan Info

Is Now a Good Time to Refinance?

Mortgage & Loan Info

How To Qualify For A VA Loan

Mortgage & Loan Info

Reverse Mortgage Pros And Cons 2025

Mortgage Texas

Current Interest Rates In Texas

Mortgage California

Current Mortgage Interest Rates In California

Mortgage Michigan

Current Home Mortgage Interest Rates in Michigan

Mortgage & Loan Info

Current USDA Mortgage Rates in the United States

Mortgage & Loan Info

How Soon Can You Refinance A Mortgage

Mortgage & Loan Info

Current Home Equity Mortgage Rates

Mortgage & Loan Info

Current Second Home Mortgage Rates

Mortgage & Loan Info

How to Refinance a Home Equity Loan: A Complete Guide

Mortgage & Loan Info

VA Construction Loan: Everything You Need to Know

Mortgage & Loan Info

When Is the Right Time to Refinance A Mortgage

Mortgage & Loan Info

What Is a VA Mortgage Loan: A Complete Guide

Mortgage & Loan Info

How To Refinance A Personal Loan: A Complete Guide

Mortgage & Loan Info

What is a Cash Out Refinance? A Complete Overview

Mortgage & Loan Info

Mortgage Rates Trends Over Time

Mortgage & Loan Info

What is an Adjustable Rate Mortgage (ARM)? A Complete Guide

Mortgage & Loan Info

Current Mortgage Interest Rates: A Detailed Guide

Mortgage & Loan Info

Current VA Mortgage Rates 2025

Mortgage & Loan Info

How To Get Preapproved For A Mortgage

Mortgage & Loan Info

What Is a Private Mortgage Insurance (PMI): A Detailed Guide

Mortgage & Loan Info

Are Property Taxes Included In Your Mortgage?

Mortgage & Loan Info

What Percentage of Income Should Go To Mortgage?

Mortgage & Loan Info

How Do I Qualify For an FHA Mortgage?

Mortgage & Loan Info

Tips to Pay off Mortgage Early

Mortgage & Loan Info

Tips to Lower Your Mortgage Payment

Mortgage & Loan Info

How Long Does It Take to Refinance a House?

Mortgage & Loan Info

Will Mortgage Rates Go Down in 2026?

Mortgage & Loan Info

What Is An Interest Rate in a Mortgage?

Mortgage & Loan Info

How Much Does It Cost To Refinance A Mortgage?

Mortgage & Loan Info

Can I Pay My Mortgage With A Credit Card?

Mortgage & Loan Info

20 Year Mortgage Rates In the United States

Mortgage & Loan Info

When Will Mortgage Rates Go Down

Mortgage & Loan Info

What Is A Mortgage Insurance: A Complete Guide

Mortgage & Loan Info

15 Year Fixed Mortgage Rates In United States

Mortgage & Loan Info

What Is A Reverse Mortgage: What You Need to Know

Mortgage & Loan Info

10-Year Mortgage Rates in the United States

Mortgage & Loan Info

How Does a VA Home Loan Work

Mortgage & Loan Info

Mortgage Rates Predictions 2025

Mortgage & Loan Info

Current 30 Year Mortgage Rates

Mortgage California

Mortgage Lenders Fremont

Mortgage California

Current Mortgage Rates Castro Valley CA

Mortgage California

Mortgage Lenders Castro Valley CA

Mortgage California

Current Mortgage Rates in Danville

Mortgage California

Mortgage Lenders Danville

Mortgage California

Current Mortgage Rates San Ramon

Mortgage California

Mortgage Lenders San Ramon

Mortgage California

Current Mortgage Rates Pleasanton CA

Mortgage California

Mortgage Lenders Pleasanton CA

Mortgage California

Current Mortgage Rates Lodi CA

Mortgage California

Mortgage Lenders Lodi CA

Mortgage California

Current Mortgage Rates Vallejo

Mortgage California

Mortgage Lenders Vallejo

Mortgage California

Mortgage Rates Roseville

Mortgage California

Current Mortgage Rates Turlock

Mortgage California

Current Mortgage Rates Merced

Mortgage California

Current Mortgage Rates Antioch

Mortgage California

Current Mortgage Rates Elk Grove

Mortgage California

Current Mortgage Rates San Leandro

Mortgage California

Current Mortgage Rates Hayward

Mortgage California

Current Mortgage Rates Brentwood

Mortgage California

Mortgage Lenders Merced

Mortgage California

Mortgage Lenders Elk Grove

Mortgage California

Mortgage Lenders Antioch

Mortgage California

Mortgage Lenders Bakersfield

Mortgage & Loan Info

Major Pros and Cons Of FHA Vs Conventional Mortgages

Mortgage & Loan Info

10 Common Mortgage Mistakes One Can Avoid While Purchasing Home

Mortgage Texas

Navigating the Houston Mortgage Market: Tips for Homebuyers

Mortgage & Loan Info

Catering To The Mortgage Needs Of Entrepreneurs And Self-Employed Borrowers

Mortgage & Loan Info

What is the Right Time To Opt For Mortgage Refinancing

Mortgage & Loan Info

How To Improve Your Credit Score For Better Mortgage Rates

Mortgage & Loan Info

Mortgage Interest Rates For First Time Home Buyers

Mortgage Texas

First Time Home Buyers Texas

Mortgage California

Loans For First Time Home Buyers In United States

Mortgage Florida

First Time Home Buyers Florida

Mortgage & Loan Info

How to Get First Time Home Buyers Loan & Grant

Mortgage Texas

Mortgage Broker Waco TX

Mortgage Texas

Current Mortgage Rates Arlington TX

Mortgage Texas

Mortgage Rates Lubbock

Mortgage Texas

Mortgage Lenders Brownsville TX

Mortgage Texas

Mortgage Rates EL Paso

Mortgage Florida

Mortgage Broker Naples

Mortgage Florida

Mortgage Broker Pensacola FL

Mortgage Florida

Current Mortgage Rates Jacksonville FL

Mortgage Florida

Current Mortgage Rates Miami

Mortgage Florida

Current Mortgage Rates In Tampa FL

Mortgage Texas

Corpus Christi Mortgage Rates

Mortgage Florida

Current Mortgage Rates In Orlando

Mortgage Florida

Mortgage Lenders Miami

Mortgage & Loan Info

VA Home Loan Interest Rates In United States

Mortgage California

Best Home Loan Lenders For First Time Buyers in United States

Mortgage Florida

Mortgage Broker Tampa

Mortgage Florida

Mortgage Broker & Lenders Orlando

Mortgage California

10 Best VA Home Loan Lenders In United States

Mortgage Washington

Marysville Mortgage Rates

Mortgage Washington

Bellingham Mortgage Rates

Mortgage California

Riverside Ca Mortgage Rates

Mortgage Washington

Current Mortgage Rates Vancouver

Mortgage Washington

Current Mortgage Rates Seattle

Mortgage Washington

Bothell Mortgage Rates

Mortgage California

Mortgage Lenders San Francisco

Mortgage Washington

Current Mortgage Rates Washington State

Mortgage Colorado

Current Mortgage Rates Denver

Mortgage Colorado

Colorado Springs Mortgage Rates

Mortgage California

Mortgage Lenders San Diego

Mortgage California

Modesto Mortgage Rates

Mortgage Texas

Mortgage Brokers Austin

Mortgage Texas

Mortgage Lenders San Marcos

Mortgage California

Mortgage Broker San Diego

Mortgage California

Best Home Refinance Companies In United States

Mortgage California

Mortgage Rates San Bernardino

Mortgage Washington

Kirkland Mortgage Companies

Mortgage Washington

Mortgage Lenders Walla Walla

Mortgage California

Mortgage Lenders Oakland

Mortgage Colorado

Mortgage Broker Colorado Springs

Mortgage California

Mortgage Rates Stockton

Mortgage California

Mortgage Brokers Stockton

Mortgage Texas

Fort Worth Mortgage Lenders & Brokers

Mortgage Texas

Mortgage Brokers San Antonio

Mortgage Texas

Mortgage Brokers Dallas

Mortgage California

Mortgage Lenders San Bernardino

Mortgage California

Mortgage Rates Fresno

Mortgage California

Top 10 Mortgage Refinance Companies In United States

Mortgage Texas

Mortgage Lenders In Amarillo TX

Mortgage California

Mortgage Broker Pasadena

Mortgage Colorado

Best Mortgage Lenders Colorado

Mortgage Florida

Mortgage Brokers Florida

Mortgage Virginia

Best Mortgage Lender Virginia Beach

Mortgage Texas

Mortgage Companies Frisco Tx

Mortgage Texas

Mortgage Companies McKinney TX

Mortgage Colorado

Mortgage Rates Colorado

Mortgage California

Mortgage Broker Roseville

Mortgage California

Best Mortgage Brokers Sacramento

Mortgage California

Fremont Mortgage Company

Mortgage California

Fremont Mortgage Rates

Mortgage Colorado

Mortgage Brokers In Colorado

Mortgage Texas

Lubbock Mortgage Lenders

Mortgage Michigan

Mortgage Rates Michigan

Mortgage California

Mortgage Broker Los Angeles

Mortgage Colorado

Aurora Mortgage Broker & Lenders

Mortgage California

Mortgage Lenders Modesto

Mortgage Colorado

Denver Mortgage Broker & Lenders

Mortgage Washington

Mortgage Broker Redmond

Mortgage Washington

Mortgage Lenders Yakima

Mortgage Washington

Mortgage Lenders & Brokers Vancouver WA

Mortgage Washington

Mortgage Broker & Lenders Issaquah

Mortgage California

Lynnwood Mortgage Brokers & Lenders

Mortgage Washington

Everett Mortgage Companies

Mortgage Washington

Mortgage Lenders Bellingham

Mortgage Washington

Mortgage Lenders And Brokers Spokane

Mortgage Washington

Mortgage Lenders Bellevue

Mortgage Washington

Mortgage Brokers Olympia WA

Mortgage Washington

Mortgage Lenders & Brokers Tacoma

Mortgage Washington

Mortgage Brokers & Lenders Seattle

Mortgage California

Mortgage Brokers in Beverly Hills CA

Mortgage California

Stockton Mortgage Brokers & Lenders

Mortgage California

Mortgage Lenders in Irvine California

Mortgage California

Mortgage Brokers Santa Monica

Mortgage California

Mortgage Brokers And Lenders In Riverside CA

Mortgage Texas

Current Mortgage Rates In Houston

Mortgage Texas

Best Mortgage Lenders In Houston

Mortgage California

Best Mortgage Lenders Sacramento

Mortgage California

Current Mortgage Rates in California

Mortgage California

Current Mortgage Rates San Diego

Mortgage California

Oakland CA Mortgage Rates

Mortgage California

Mortgage Rates Bakersfield

Mortgage California

Mortgage Rates In San Jose

Mortgage California

Current Mortgage Rates San Francisco

Mortgage California

Current Mortgage Rates Sacramento

Mortgage California

Current Mortgage Rates Los Angeles

Mortgage California

Mortgage Lenders & Brokers San Jose

Mortgage California

Mortgage Lenders Los Angeles

Mortgage California

California Mortgage Lenders & Brokers

Mortgage California

Best Mortgage Companies in San Francisco

Mortgage California

Top Mortgage Companies in Santa Cruz

Mortgage California

Mortgage Companies in Newport Beach

Mortgage California

Mortgage Lenders Fresno

Mortgage Texas

Current Mortgage Rates Fort Worth

Mortgage Texas

Mortgage Lenders In Austin

Mortgage Texas

Mortgage Rates In Austin

Mortgage Texas

Mortgage Lenders El Paso

Mortgage Texas

Mortgage Companies Plano

Mortgage Texas

Arlington Mortgage Brokers

Mortgage Texas

Mortgage Lenders Corpus Christi

Mortgage Texas

Mortgage Lenders Houston

Mortgage Texas

Current Mortgage Rates in Dallas

Mortgage Michigan

Best Mortgage Lenders in Michigan

Mortgage Texas

Best Mortgage Lenders Dallas

Mortgage Washington

Best Mortgage Lenders In Washington State

Mortgage Texas

Mortgage Lenders in San Antonio

Mortgage Texas

Mortgage Rates In Texas

Mortgage Texas

Best Mortgage Lenders In Texas

Mortgage Colorado

Best Mortgage Companies In Colorado Springs

Mortgage Florida

Mortgage Companies In Fort Lauderdale Florida

Mortgage Florida

Best Mortgage Lenders in Florida

Mortgage Virginia

Mortgage Companies in Virginia

Mortgage Texas

Current Mortgage Rates in San Antonio

Mortgage Florida

Mortgage Rates in Florida

Mortgage Virginia

Best Mortgage Rates in Virginia

Mortgage California

Best Refinance Companies in California